2 Big Reasons Banks Will Be Holding Excess Cash in 2022

People are holding onto their money, businesses are in a holding pattern, and banks are seeing a drop in lending activity.

Those are the basic conclusions of a recent 2022 Banking Industry Outlook report released by S&P Global Market Intelligence. Their study analyzes current trends in banking behavior and uses those patterns to try and forecast what we can expect as we move into the new year.

Bank Balance Sheets Heavy With Excess Liquidity

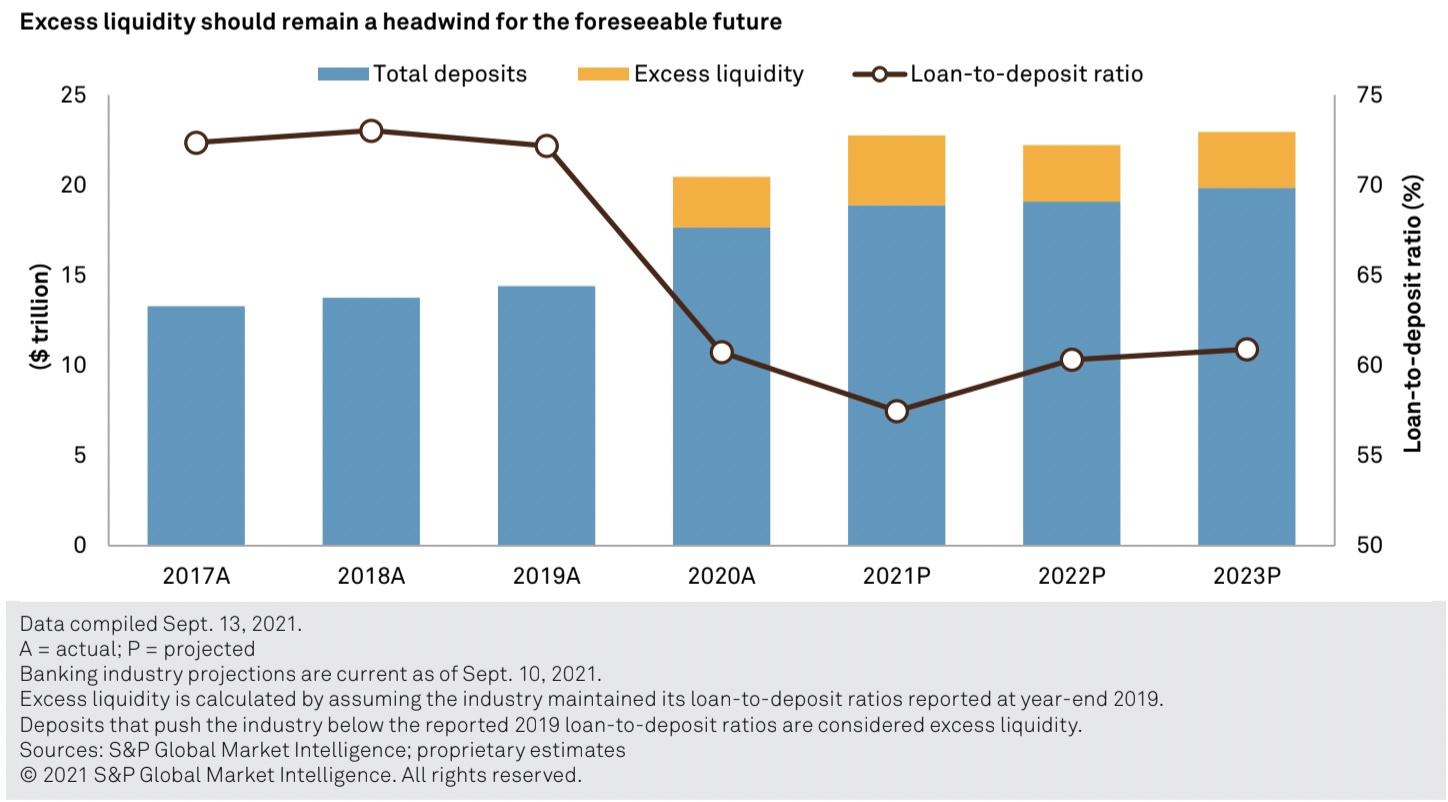

During the height of the COVID-19 pandemic throughout 2020, the U.S. government pumped an extremely large amount of cash into the market. This created a difficult situation for many banks.

First, many people who would have ordinarily taken out loans to fund some of their activities last year did not need to borrow the money. They may have been working from home, and, therefore, had lower expenses related to work, commuting, etc. They may have also seen extra cash flow into their bank accounts due to stimulus money from the federal government. As a result, individual bank customers didn’t borrow as much money as in years past.

As soon as the nation shut down because of COVID, people started holding onto their money. Banking analysts aren’t expecting that trend to change anytime soon.

This is evident in the data that shows increased savings rates during 2020. According to S&P Global, the monthly savings rate last year equaled or exceeded 9% nearly every month since March. (By comparison, the savings rate only passed 9% four times between 2000 and 2020!)

Second, these funds are not generating much interest income because banks weren’t making as many loans. This resulted in excess liquidity that banks aren’t typically used to having.

What Excess Liquidity Means for Most Banks

Banks are in the business of loaning money, and they generate most of their income from interest payments. Having large amounts of excess cash on hand is the equivalent of a retail store having lots of inventory on the shelves and no customers coming in the door.

S&P Global predicts that banks will continue to realize “little to no earnings growth over the next few years.” Smaller banks that have not found ways to pivot to new technologies during the pandemic will especially feel the pinch.

New Competition Means Banks Need to Adapt

Moving forward, banks will not be able to do “business as usual” and expect to thrive. New “fintech” (financial technology) companies have sprung up over the past few years that are challenging the traditional ways that customers interact with their money.

People are getting more and more comfortable using their smartphones and other technology to conduct banking transactions digitally. Being locked down for much of 2020 and unable to conduct many transactions in person has only accelerated that trend.

Look for fintech companies to take a larger and larger market share of banking, investing, and lending in the future. Many of these companies are startups, but larger financial institutions are finding ways to provide these services to their customers as well. Smaller banks would do well to adjust their practices in order to keep from losing customers to remote ways of banking.

Southard Financial Can Help You Make the Shift

We have been helping clients monitor and understand changing financial markets for over 30 years, and we understand how important it is to stay on top of trends like these.

Our team can provide a variety of Services for Financial Institutions including appraisals, consulting, and transaction advice.

Schedule a call to learn more and discover how we can help you stay on top of an ever-changing marketplace!